A Little More Patience Required For Gold Bulls

The fundamental picture

For the short to medium-term fundamentals that influence the gold price - primarily the likes of real yields and the dollar - the outlook is still somewhat mixed for gold, after what has been a terrific year for the sector.

While it seems increasingly likely real yields are nearing their peak for this cycle, and although they are not likely to return to negative territory in the immediate future (that is more likely a story for 2024), the headwind from real yields that has kept a lid on the gold price for the last two-plus years is reaching its crescendo.

The fact that the sector has held up so well in spite of the biggest spike in real yields in decades re-affirms the bullish long-term case for gold. However, it must during the pre-QE era (when real yields were persistently positive), the relationship between gold and real yields was almost insignificant. This perhaps helps to partly explain why precious metals have held up relative well during this period.

Nonetheless, as I have pointed out in previous musings, real yields tend to follow the business cycle (at least to some degree). Of course, the relationship between yields and economic growth is not likely to be as strong as it has been in recent decades due to changing structural factors such as (potentially) higher inflation of a secular basis and a persistent oversupply of US Treasuries, real yields should at some point soon head lower. Though for this to occur, we likely need a more dovish tone from the Fed, and I suspect we are not quite there yet.

Expecting rate cute before 2024 seems highly unlikely in my book, but historically the gold price has reacted positively once rate cuts commence.

Regardless, gold and the precious metals sector tend to perform relatively well as we reach the latter stages of the business cycle - of which we are likely in or entering.

And although it remains far too early for rate cuts, the conditions for a significant move higher in precious metals are slowly coming together. An inverted yield curve is another such example.

This year’s price action certainly attests to this notion, but, the ideal conditions for a significant move higher are likely not yet in place.

Indeed, one variable that leads me to remain somewhat cautious on the sector for the time being is the dollar. My outlook for the dollar hasn’t really changed since I detailed my thesis back in January. Put simply, I remain neutral to bullish the dollar over the next few quarters, and generally bearish on a cyclical perspective. And, while they don’t always trade inversely, a spike in the dollar is most probably going to put pressure on the precious metals market. I think this remains a material risk for the time being.

Indeed, if we examine the technical picture for the dollar, it appears the daily chart is forming somewhat of a bullish flag pattern after a false breakdown below the $100 support level. This is bullish price action in my view. Thus, I can’t help but think the dollar goes higher at some point in the near future, and retaking the 200-day moving average and breaking out above the $103-$104 level on the dollar index would probably confirm this notion. This would not guarantee a precious metals correction, but is likely to put pressure on the sector.

As it stands, another move higher in the dollar could see the gold price continue this period of consolidation and/or correction for a little while longer. But, when the dollar does roll over, I expect this bull market in precious metals to continue in earnest. A little more patience is required for gold bulls for the time being.

Sentiment and positioning

From a sentiment and positioning perspective, the signalling is again somewhat mixed. Managed money positioning in gold futures currently lies in the middle of its recent historical range, suggesting speculative positioning is neither overly bullish nor overly bearish and in the process is giving no clear contrarian signals.

Sentiment on the other hand is perhaps a little more constructive. The fact that gold recently tested its all-time highs amid very little fanfare or media coverage is absolutely bullish.

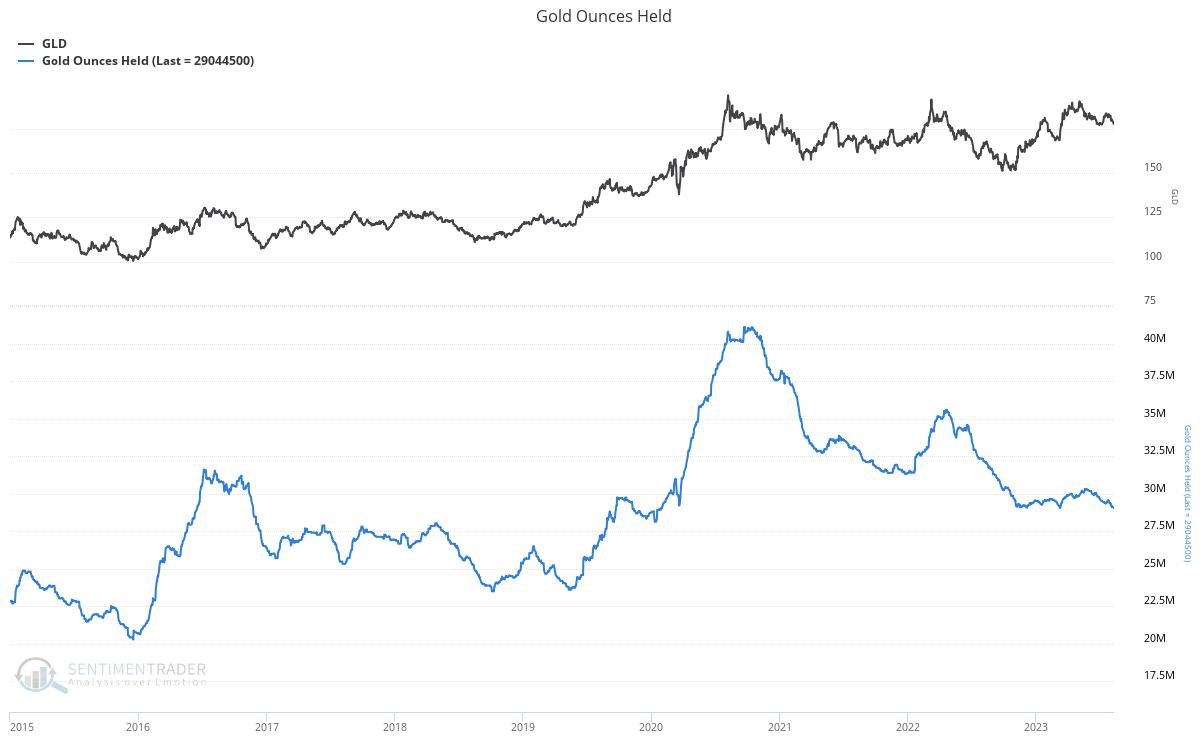

Indeed, if we assess sentiment via such measures as flows into the GLD ETF, we can see how the recent highs were actually accompanied with only mediocre flows. This illustrates how the precious metals market is not anywhere close to exhibiting the kind of speculative furore evident at most market tops, while the fact that this correction has also seen meaningful outflows from gold ETFs is also of great encouragement to the medium-term outlook for the yellow rock.

A similar message can be gleaned from looking at the actual gold ounces held by the various physical gold ETFs, which despite the gold price flirting with all-time highs, physical gold held by ETFs is flirting with four-year lows.

While other sentiment measures such as the Daily Sentiment Index (DSI) per the below is looking to be reaching levels seen at market lows (though this metric could still go lower short-term).

Source: The Felder Report

While speculative positioning may not be providing any meaningful signal at present, sentiment remains far from any level indicative of a meaningful top in prices. This paints an encouraging picture for the outlook for precious metals in 2023 and 2024 once the rally resumes.

Central banks keep on buying

One of the primary factors keeping a floor on the gold price over the past couple of years has been the activity within the physical market, primarily through the actions of central banks.

The diversification of FX reserves into gold is of course one of the primary long-term fundamental reasons for owning gold, and it seems this trend continues to play out as all gold bulls have hoped.

Indeed, their continues to be some tightness at the front end of the gold futures term structure - suggesting physical demand remains. Although the front-end of the curve is longer in backwardation as it was during much of 2022 and early 2023, it is still exhibiting tightness, which is not a common occurrence within the gold market as demand for physical delivery of the commodity is little given gold’s lack of utility as a physical commodity.

This is perhaps better illustrated by looking at the front month prompt spreads, which as we can see below, have diverged positively from price to a significant degree.

Market technicals

From a technical perspective, the price action for gold continues to look favourable as higher highs and higher lows have been the norm since the market bottomed late last year. Whether this pull-back will see the gold price fall below the $1,940 support area remains a possibility, but I do believe any move lower toward $1,865 or even the $1,800 level should be considered an excellent buying opportunity for gold bulls.

Seasonality also remains pretty favourable over the next quarter, lending credence to the idea this pull-back may actually be done for now, though I am somewhat sceptical.

As it stands, the outlook for precious metals over the short to medium-term remains somewhat mixed for now. Although real yields are likely reaching their peak (though by all means could go higher over the short-term), continued hawkish Fed policy and the potential for a renewed rally in the dollar will likely put a cap on gold prices for the time being. The conditions are still probably not yet in place for a significant upward move in gold, thus I can’t help but think the next big move may still be a story for 2024 rather than 2023, though the long-term outlook for the sector remains positive and any material dips should be bought by those bullish the sector.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.