Now Is Not The Time To Buy Bonds

Summary & Key Takeaways

The fundamental outlook for bonds remains questionable at best.

The leading indicators of growth and inflation for 2024 suggest both dynamics could put upside pressure on yields.

Sentiment toward bonds remains bullish as the consensus is for yields to move lower. However, given hedge funds and CTAs are short bond futures, there is of scope for a squeeze higher, but it will likely prove temporary.

For a significant rally in long-duration bonds to occur, we need to see a deep recession (which will likely be driven by a material rise in unemployment), a stock market crash or strong disinflationary push in 2024 (unlikely to occur without a recession).

Now is not the time to be piling into long-duration bonds, particularly when short-term fixed interest securities are offering more attractive yields without any duration risk.

Growth and inflation are not supportive of bonds

On both a secular and cyclical basis, I am a bond bear. I last wrote about bonds in September, laying out why I believe bonds represent a poor risk-reward investment on almost all time frames. Yields are flat to slightly highly since I penned this piece, and unsurprisingly, my view has changed little.

From a growth and inflation perspective, now is not the time to be overweight duration. As we can see below, growth surprises and inflation surprises continue to be positive, as has been the case for the past few months. These are not conditions supportive of a meaningful rally in bonds.

The same can be said when we compare my inflation leading indicator versus the ISM Manufacturing New Orders less Inventories spread, an excellent short-term leading indicator of economic growth. Although this metric was a little more favourable toward bonds at certain points in 2022 and 2023, these variables are currently pointing to an underweight exposure to duration.

Clearly, we are yet to experience any prolonged period whereby growth and inflation decline in unison. As we can see below, such conditions are clearly the most favourable for bonds. Instead, much of 2023 saw falling inflation and rising growth, hence why bonds have been unable to rally on a sustainable basis. While 2024 has thus far seen both upside growth and inflation pressures.

As a result of these dynamics, yields struggled to move materially lower in 2022 and 2023 in-line with the manufacturing cycle as historically has been the case. The ISM Manufacturing PMI bottomed months ago now, suggesting any negative growth impulse that was a tailwind for bonds has come and gone.

This is exactly what the leading indicators of the business cycle are suggesting. Both my Compositing Leading Economic Index and Macro Conditions Index have been suggesting for some time now 2024 will be the year we see a strong rebound in the business cycle. This is a negative for bonds as we saw above, as accelerating growth puts upward pressure on yields. Barring any imminent recession fuelled via a spike in unemployment (unlikely for now), the economic growth impulse appears a headwind for bonds moving forward.

On the inflation front, the tailwind for bonds (and headwind for yields) that has been disinflation over much of the past 18 months is seemingly coming to an end. Not only has the downtrend in inflation losing steam, but upside momentum in inflation since the turn of the year has clearly surprised to the upside.

What’s more, my inflation leading indicator continues to suggest modest upward pressure on CPI will continue over the coming six months.

Now, I don’t believe inflation will move materially higher from here and it is likely we see further disinflation over the short-term, I believe it more likely we see Headline CPI above 4% than we do below 2% at any point this year. Again, upward pressures on inflation are a headwind for bonds, and conversely a tailwind for yields.

As a result, one could easily make the case yields are actually undervalued at current levels (bonds overvalued). Indeed, if we compare the historical relationship between GDP and yields (though an admittedly dubious one), yields are currently far below levels of where they should be in an economy running ~6% nominal GDP.

Perhaps a more meaningful comparison is Treasury yields and mortgage yields. Mortgage yields generally trade at a slight premium to Treasury yields, but, as we can see below, that premium is near the largest in history, suggesting Treasury yields are either too low relative to mortgages or vice versa. Given where growth and inflation currently sit and the outlook for both, it seems more likely Treasury yields may be undervalued.

What is interesting however is market internals are not pointing to higher yields at present. Indeed, my model of market internals, which incorporates measures such as copper/gold ratio, cyclicals/defensives ratio and regional banks/utilities ratio among others, tends to given an indication of where the market believes yields should be trading, and has disconfirmed the recent high in yields.

If we break out these measures individually as I have done below, we can see my model is being skewed lower by the recent outperformance of gold relative to copper (even though copper is moving higher), along with regional banks continuing to trade poorly on the back of deposit outflow risk and ongoing fears of future regional bank failures.

Alas, one could make the argument my market internals model is being skewed lower via factors that are unrelated to yields themselves. However, I try not to rationalise any indicator and will take this at face value, thus, it appears likely yields may have moved too high in the short-term, and may need to correct lower before they are able to move higher as the medium-term fundamentals suggest they should. Any further disinflationary data over the next few months will likely offer a short-term reprieve for bonds.

Sentiment and positioning

From a positioning standpoint, we remain at an interesting conundrum. As we can see below, asset manager positioning toward bonds is close to decade highs, while leveraged fund positioning (i.e. hedge funds and CTAs) remains near decade lows.

Beginning with asset managers, while they are nearly as long bonds as they have been at any point in the last decade, we can clearly see their positioning levels provide little insight from a contrarian perspective.

Leveraged funds on the other hand seemingly provide a much more informative contrarian signal. That is, they have historically been the drivers of market moves and are thus short at the bottoms and long at the tops. However, while it is true they are currently short Treasury futures to their largest extent in a decade, we must keep in mind part of this positioning comes as a result of the basis trade hedge funds have been piling into in the last couple of years. As explained in detail here, the basis trade involves hedge funds selling Treasury futures and buying the underlying physical Treasuries, profiting from the spread that has opened up between the two as a result of institutions and pension funds bidding up the underlying (relative to futures). Thus, hedge funds may be short futures, but their actual net positions may not be quite so bearish when taking into account their long underlying positions.

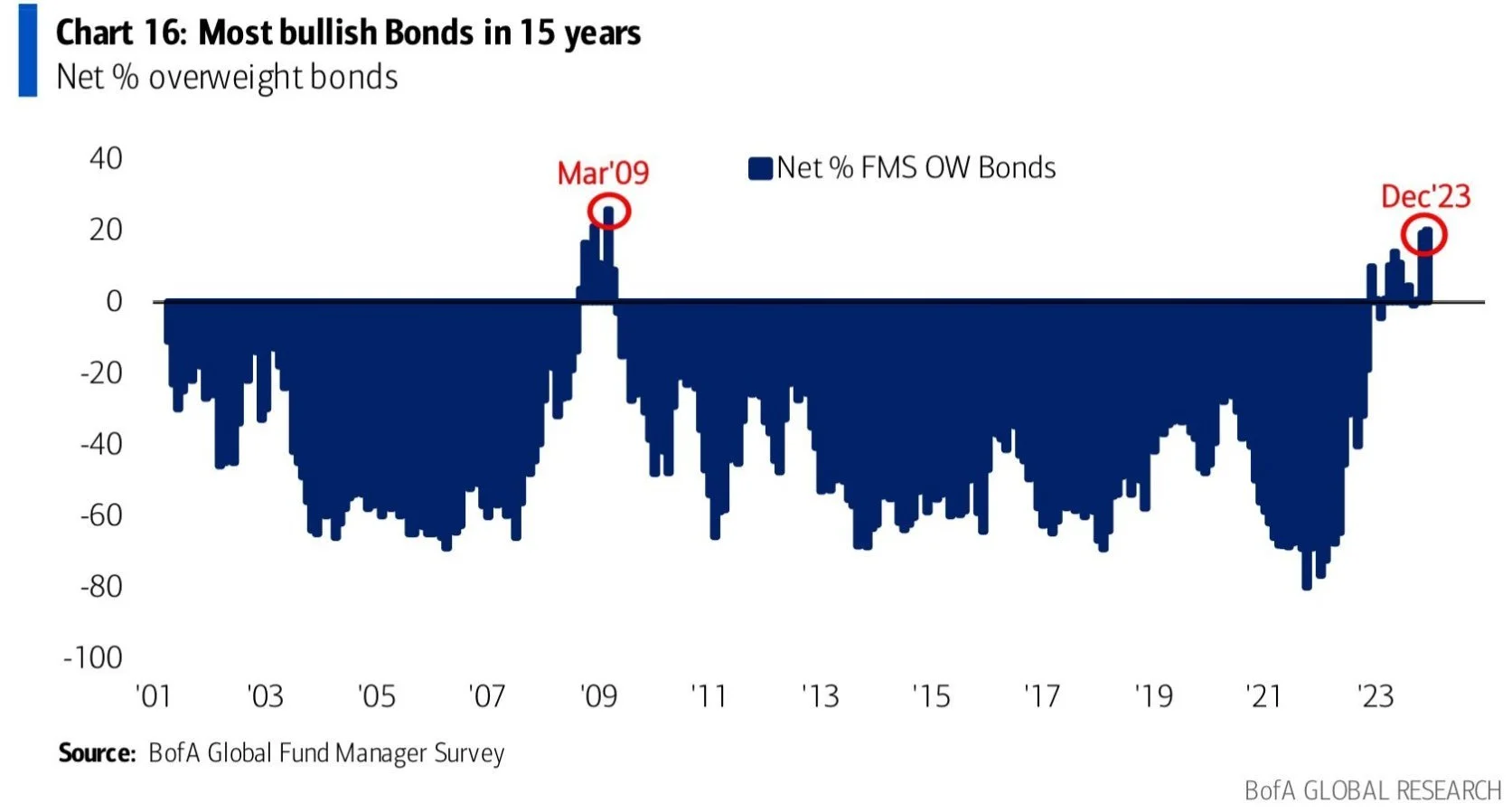

If we delve a little deeper into positioning, there clearly remains a bullish consensus toward bonds from fund managers. Per Bank of America’s Global Fund Manager Survey, managers are heavily overweight bonds and are as bullish toward the asset class as they have been since 2009 (a point which marked the top in bonds for that cycle).

Clearly, the consensus is for rates to move lower, not higher.

From a CTA positioning standpoint however, it is fair to say there remains plenty of upside risk here. The below chart is the current asset class breakdown for the DBMF ETF, which is a managed futures ETF whose positions mimic that of trend following CTAs, and thus acts as a proxy of how CTAs are currently positioned. As we can see, CTAs are heavily short fixed income at present. At some point they will need to buy back these positions, which means the downside for bonds is likely to be somewhat limited for the time being.

Source: iMGP Funds

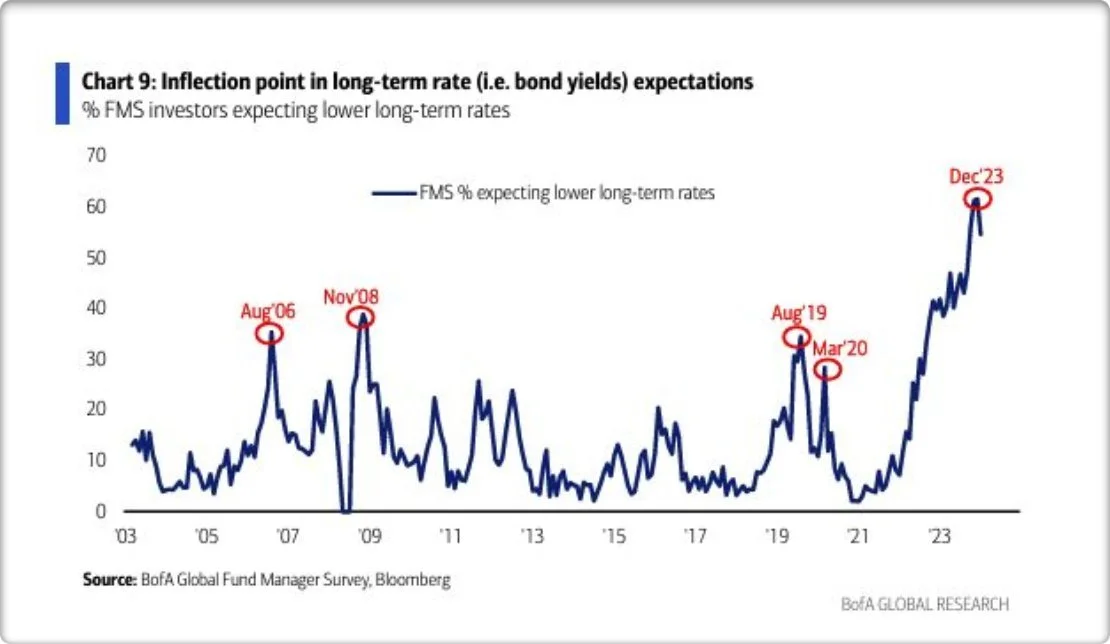

From a sentiment perspective, the message is largely similar to positioning. Some measures of sentiment are now longer at the bullish extreme they were last year, at least in terms of fund flows into TLT, which have fallen back to neutral levels over the past couple of months. However, when we look at TLT short interest, this remains close to decade lows, and is generally near levels you see at cyclical tops in bonds, not bottoms.

When we look at other survey-based sentiment measures such as the Conference Board Bond Survey (which measures the net percentage of consumers expecting bond prices to rise), we can see there is presently an extreme bias toward bond bullishness.

In summary, sentiment toward bonds remains relatively bullish, while certain areas of positioning are less so. Thus, given hedge funds and CTAs are short bond futures, there is plenty of scope for a squeeze higher, but it will likely prove temporary as asset managers and fund managers are already well and truly long bonds and any move higher is unlikely to be supported by fundamentals.

The supply and demand problem could find cyclical reprieve, but structural issues remain

The supply and demand outlook for bonds over the long-term (think five to 10 years) is one of the primary reasons why I remain bearish. However, on a short-term basis, we could be in for a reprieve on the supply front.

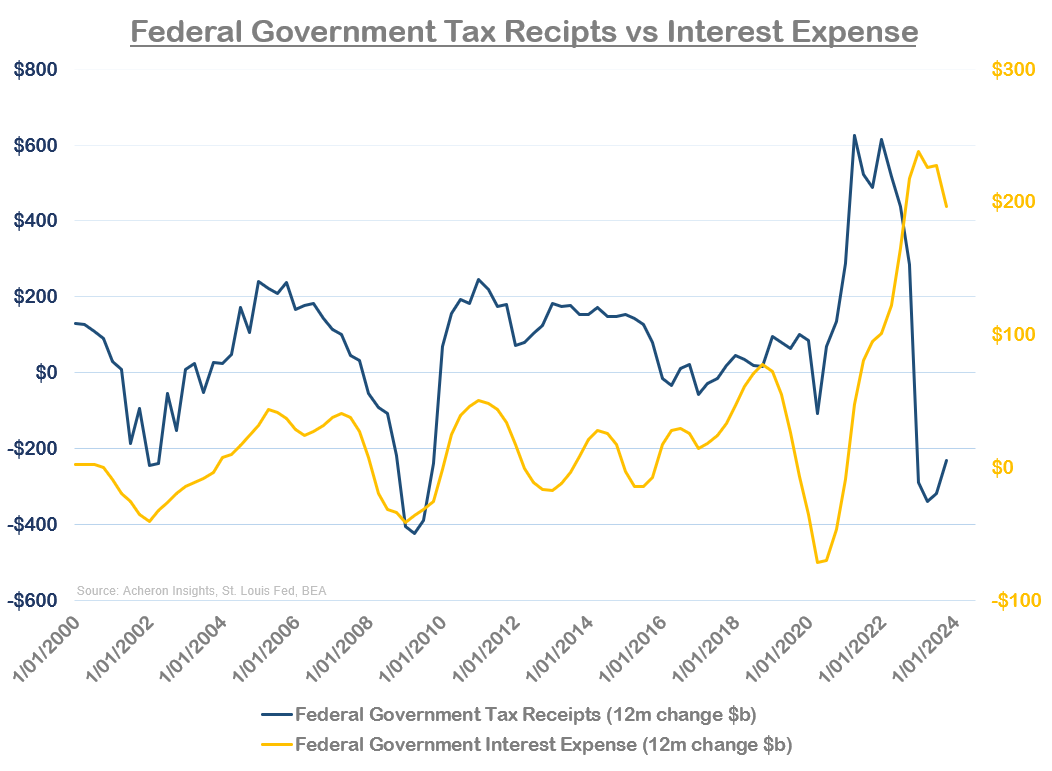

What’s been a significant driver of debt issuance from the US Treasury in recent times has been falling tax receipts and rising interest costs, as is illustrated in the below chart.

Of course, interest costs of the US government are a function of bond yields, with all tenors now sitting well above 4% and the short-end over 5%. But, when we compare the 12-month change in the 10-year Treasury yield relative to the 12-month change in government interest payments, the latter should find some reprieve over the next quarter or two as bond yields have largely moved sideways in recent times.

Conversely, federal tax receipts are also likely to move higher through Q2 and Q3, following the move higher in asset prices.

Given how financialised the United States’ economy has become and the link between stock prices, employment, incomes and capital gains tax, the boom in stocks over the past year will significantly boost federal tax receipts.

These combined factors should result in a reduced need for Treasury issuance over the coming quarters, something which the Treasury’s Quarterly Refunding Announcement seemed to indicate.

As a result, less net issuance means less supply. How much of an impact this actually have for bonds remains to be seen (as the Treasury is still set to issue around ~$500b in debt through Q2), but is worth highlighting nonetheless.

On the other side of the coin however is the constituents of the debt issuance and the percentage of the deficit being funded via short-term bills versus longer-dated bonds. Historically, the Treasury has generally favoured issuing a greater level of bonds versus bills, but in recent years due to the build-up of the Reverse Repo Facility (RRP), Yellen has been issuing a greater level of bills versus bonds which are effectively being funded via the RRP and offsetting almost all the Fed’s QT program since late 2022.

Unfortunately, the RRP has been drained significantly, leaving little room for the deficit to be funded via its drawdown moving forward. Thus, should Yellen and the Treasury normalise the proportion of coupons they issue relative to bills (inevitable at some point), this would potentially put greater upside pressure on long-term yields.

And again, while debt issuance may fall for a short period this year, the demand and supply mismatch remains a headwind for bond term premium and thus long-duration bonds.

Source: CrossBorder Capital

Putting it all together

In summary, the fundamental outlook for bonds remains questionable at best. For a rally in long-duration bonds to occur, we need to see a deep recession (which will likely be driven by a material rise in unemployment), a stock market crash or strong disinflationary push in 2024 (unlikely to occur without a recession). Yes, there is the potential for some form of short-term rally in bonds driven by CTA buying, but given the outlook for growth and inflation, that would likely be fleeting.

In addition, even if the Fed is able to cuts rates this year, if this occurs in a growth cycle upturn while inflationary pressures re-emerge, that would only put further upside pressure on interest rate term premium.

As such, while yields may not necessarily move higher in the near-term, it appears now is not the time to be piling into long-duration bonds a la the 1990-2020 playbook. After all, why take any duration risk when you can buy short-term fixed income securities at a higher yield and much lower risk.

. . .

Thanks for reading!

If you would like to support my work and continue to allow me to do what I love, feel free to buy me a coffee, which you can do here. It would be truly appreciated.

Regardless, feel free to share this with friends and around your network. Any and all exposure goes a long way and is very much appreciated. Thanks again.